|

|

Alternative Financial Services Metros Vary Widely in Household Use of High-Cost Alternative Credit ProductsThe Great Recession has strained the finances of American households at all income levels. Households cope in a variety of ways: cutting unnecessary expenses, turning to friends, relatives, or charitable organizations for help, applying for means-tested public benefits, or borrowing funds. Those with adequate credit standing may take out loans from mainstream financial institutions: banks, credit unions, or thrift institutions. Others, either out of necessity or preference, seek credit from organizations that operate in the alternative financial services (AFS) sector. These alternative forms of credit come with high fees and charges. For example, interest rates on payday loans are in the range of 400 to 450 percent, on an annual percentage rate (APR) basis. The January 2009 supplement of the Current Population Survey (CPS) on the unbanked and underbanked constitutes one of the few national datasets tracking the use of these credit products. This FDIC-sponsored and Census-administered survey collected data on why and how frequently people turn to the following four types of AFS credit products: 1

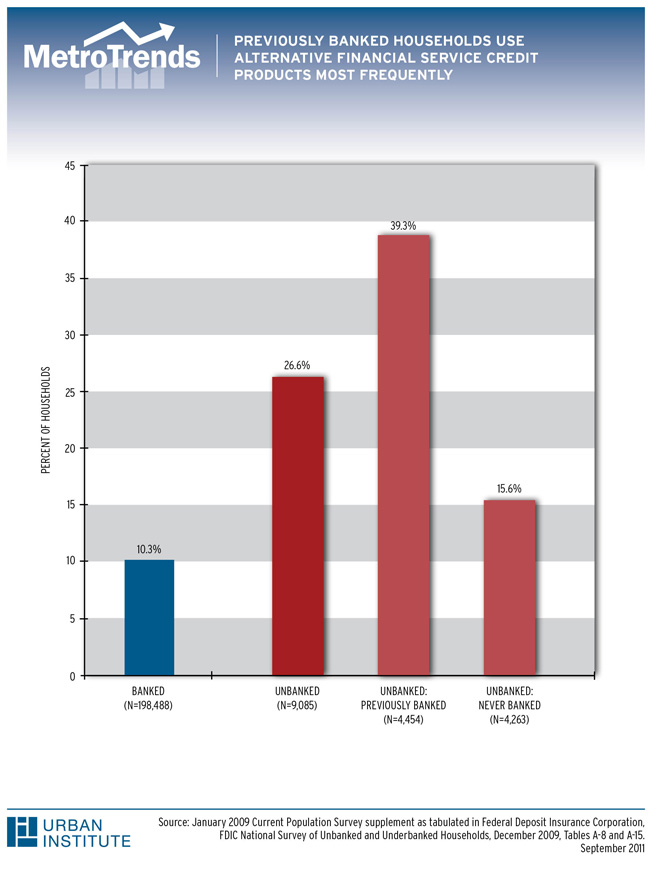

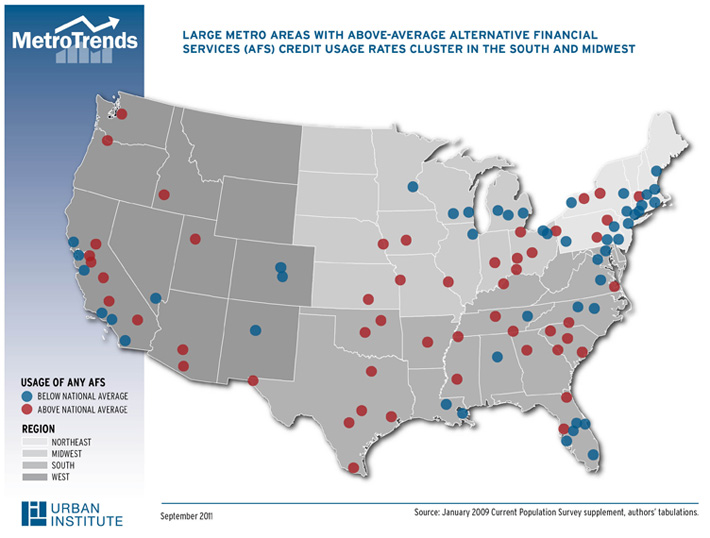

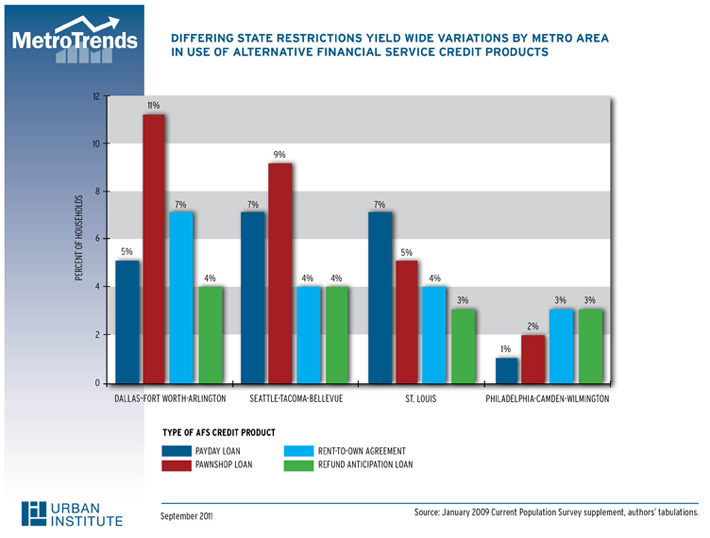

Nationally, the 2009 FDIC survey data indicate that 12 percent of U.S. households have ever used one or more of the four AFS credit products, as displayed in the graph below. Among the 8 percent of unbanked American households in which no one holds a checking or savings account, the usage rate for alternative credit products is 27 percent: more than twice as high as the 10 percent for banked households. That said, there is substantial variation among unbanked households. For those that previously held bank accounts but have lost them, the usage rate registers much higher than for those who have never been banked at all (39 versus 16 percent). This previously banked subpopulation includes many with low incomes who cite not having enough money to need the account most often as their reason for closing their prior account. Among the top 100 metro areas, 51 metros register AFS credit usage rates above the national average. Areas of high AFS credit usage cluster in the South, Midwest, and West regions of the country, as shown in the map below. When we focus on the 20 largest metro areas, where the CPS sample design allows reliable estimates, we see many of the same trends. 2 Four of the 7 metros in the South have credit usage rates above the national average, compared to 3 of 6 in the West, 1 of 4 in the Midwest, and 0 of 3 in the Northeast. Usage rates vary more than four-fold among these 20 metros, from a low in Boston (4 percent) to a high in Dallas (19 percent). To illustrate the different patterns of product use across major cities, consider the top-ranking large metros in the South, West, Midwest, and Northeast: Dallas (19 percent), Seattle (15 percent), St. Louis (14 percent), and Philadelphia (7 percent), respectively. For Dallas and Seattle, use of pawnshop loans drives AFS usage overall. These two metros have the highest usage of these products among all 20 areas (at 11 and 9 percent, respectively). Texas and Washington (unlike the majority of states) do not apply monthly interest rate caps or other regulations that restrict the availability of pawnshop loans. The low AFS credit usage rates in Northeast metros like Philadelphia reflect the fact that seven of the nine states in this region (all but New Hampshire and Rhode Island) have effectively banned payday lending through state usury laws. The other jurisdictions to have done so nationally are in the South (the District of Columbia and four of 16 states: Georgia, Maryland, North Carolina, and West Virginia) and in the West (one of 13 states: Oregon). Similarly, variation by metro area in the use of RTO agreements and RALs also result from differing state restrictions, including APR caps and disclosure requirements. It will be important to follow the trends in these AFS usage rates over the course of the recession and recovery. The Census administered the supplement again in June 2011, and the data will be released in the summer of 2012. The newer estimates will reflect the much weaker labor market that had evolved by mid-2011, emerging policy developments that restricted the availability of some AFS credit products (most notably, RALs), plus conditions in mainstream financial markets (lower interest rates, but tightened underwriting) that may have influenced the uses of credit in the AFS sector.

|

Experts

Research Assistant Center on Labor, Human Services and Population Feedback

Send us your comments to help further the discussion. Share

Commentaries

|

Gregory Mills

Gregory Mills